Table of Contents

- Mortgage Basics in Plain English

- How Much House Can You Afford?

- Pre‑Qualification vs Pre‑Approval

- Rates, Terms & Types of Mortgages

- Down Payment, PMI & Loan‑to‑Value

- DTI, Credit Scores & Automated Underwriting

- Amortization, APR & Total Cost

- Closing Costs & Cash‑to‑Close

- When (and When Not) to Refinance

- Biweekly & Extra Payments

- Prepayment: Smart Strategies

- Regional Notes & Special Programs

- Red Flags & Common Mistakes

- Step‑by‑Step Checklists

- Mortgage Glossary (Human‑Friendly)

- FAQs

- More Reading on Proculator

Mortgage Basics in Plain English

Let's start with the basics. A mortgage is essentially a long‑term loan specifically designed for purchasing property. You borrow a large amount of money (called the principal), agree to pay a certain interest rate, and repay the loan over a set number of years (known as the term). The property itself serves as collateral, which means if you stop making payments, the lender can take possession of the home through a process called foreclosure. It's the not-so-fun part of homeownership, but understanding this reality helps us make smarter decisions about choosing a mortgage that fits comfortably within your life.

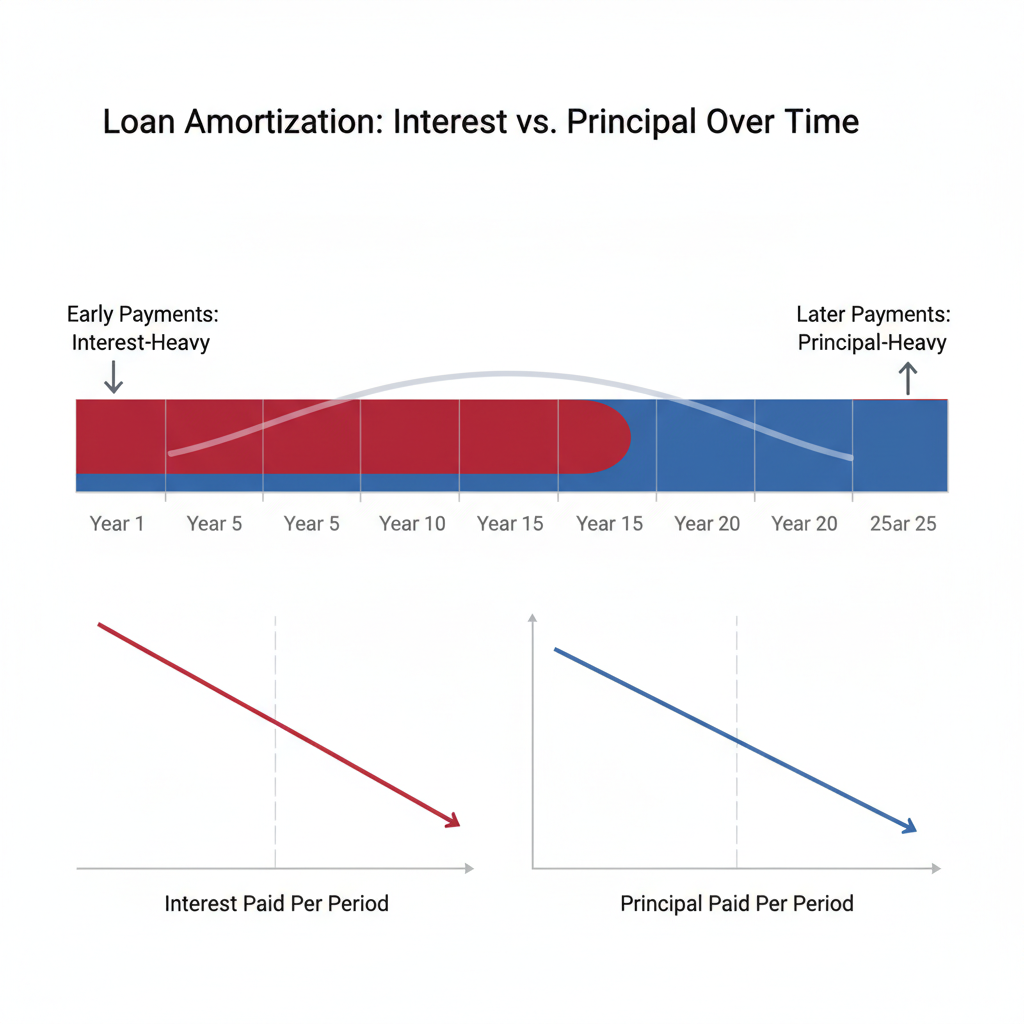

Most home loans are amortizing, which is a fancy way of saying that your regular monthly payments cover that month's interest first, then whatever is left goes toward reducing the principal. In the early years of your mortgage, interest makes up a bigger portion of each payment. As time goes on, more of your payment goes toward the principal. This is why making extra payments early in your mortgage can be incredibly powerful—you're attacking the principal when it's most vulnerable to interest accumulation.

What really determines your monthly payment?

Your mortgage payment isn't just about the loan amount and interest rate. Several factors come into play:

- Loan amount: This is the home price minus your down payment (and sometimes minus any seller credits you negotiate).

- Interest rate: This can be fixed or adjustable, and it's influenced by your credit profile, loan type, and current market conditions.

- Term: The 30-year mortgage is most common because it offers lower monthly payments, while a 15-year term has higher payments but saves you tens of thousands in interest over the life of the loan.

- Taxes & insurance: Property taxes and homeowners insurance are often escrowed (collected as part of your monthly payment and held in a separate account until they're due).

- Mortgage insurance: If your down payment is below 20% on most conventional loans, you'll likely pay Private Mortgage Insurance (PMI), which protects the lender if you default.

It's worth noting that your mortgage payment is probably the largest recurring expense you'll have, but it's not the only cost of homeownership. You'll also need to budget for maintenance, repairs, potential HOA fees, and unexpected emergencies. A good rule of thumb is to set aside 1-2% of your home's value annually for maintenance and repairs.

The Emotional Side of Home Financing

Beyond the numbers, it's important to acknowledge the emotional weight of a mortgage decision. For most people, their home represents security, stability, and a place to build memories. The financial commitment can feel overwhelming, especially for first-time buyers. It's completely normal to feel a mix of excitement and anxiety throughout the process.

I always advise clients to separate the emotional attachment to a specific house from the financial practicality of the mortgage. You might fall in love with a home that stretches your budget too thin, and that's when difficult decisions need to be made. Remember: there will always be other houses, but financial stress can linger for years if you overextend yourself.

The key is finding a balance between your heart and your head—a home that you love that also fits comfortably within your financial life. This guide will help you navigate that balance with confidence.

How Much House Can You Actually Afford?

This is the million-dollar question (sometimes literally!). Affordability isn't just about what the bank will approve—it's about what lets you sleep at night without financial anxiety. Lenders often look at two debt‑to‑income ratios (DTI): the front‑end ratio (housing costs only) and the back‑end ratio (housing + all monthly debts). As a rule of thumb, aim for a total DTI below 36% if possible, though many loans allow higher limits, especially for borrowers with strong credit profiles.

But here's the reality check: just because you can borrow a certain amount doesn't mean you should. I've seen too many families become "house poor"—owning a beautiful home but having no money left for vacations, savings, or even unexpected expenses. Your mortgage payment should leave room for life to happen.

Real-life example: The Johnson family

Let's make this practical. Suppose the Johnson household has a gross income of $7,000/month, and they have $500 in other monthly debts (car payment, student loans, credit cards). Targeting a conservative 28% front‑end ratio means keeping housing costs near $1,960/month. If taxes and insurance are estimated at $360/month, they'd want principal + interest to be around $1,600.

With a 30‑year loan at a competitive rate (let's say 6.5%), that translates to a loan amount of approximately $250,000. Add a 10% down payment ($27,800), and they'd be looking at homes around $278,000. This is the kind of realistic math that prevents disappointment down the road.

The Hidden Costs of Homeownership

When calculating affordability, many first-time buyers focus solely on the mortgage payment while overlooking other significant expenses. Beyond your principal, interest, taxes, and insurance (PITI), you should budget for:

- Utilities: If you're moving from an apartment to a house, your utility bills will likely increase, especially for heating and cooling.

- Maintenance and repairs: As mentioned earlier, budget 1-2% of your home's value annually. A $300,000 home would need $3,000-$6,000 set aside each year.

- Homeowners Association (HOA) fees: If your property is in a managed community, these can range from $100 to over $500 per month.

- Furnishings and updates: That empty room will need furniture, and you'll likely want to personalize the space with paint, window treatments, etc.

- Increased commuting costs: If your new home is farther from work, factor in additional gas, tolls, or public transportation expenses.

I recommend creating a mock budget with all these expenses included before you start house hunting. Live with that budget for a couple of months to see how it feels. If it's uncomfortably tight, you might want to adjust your price range downward.

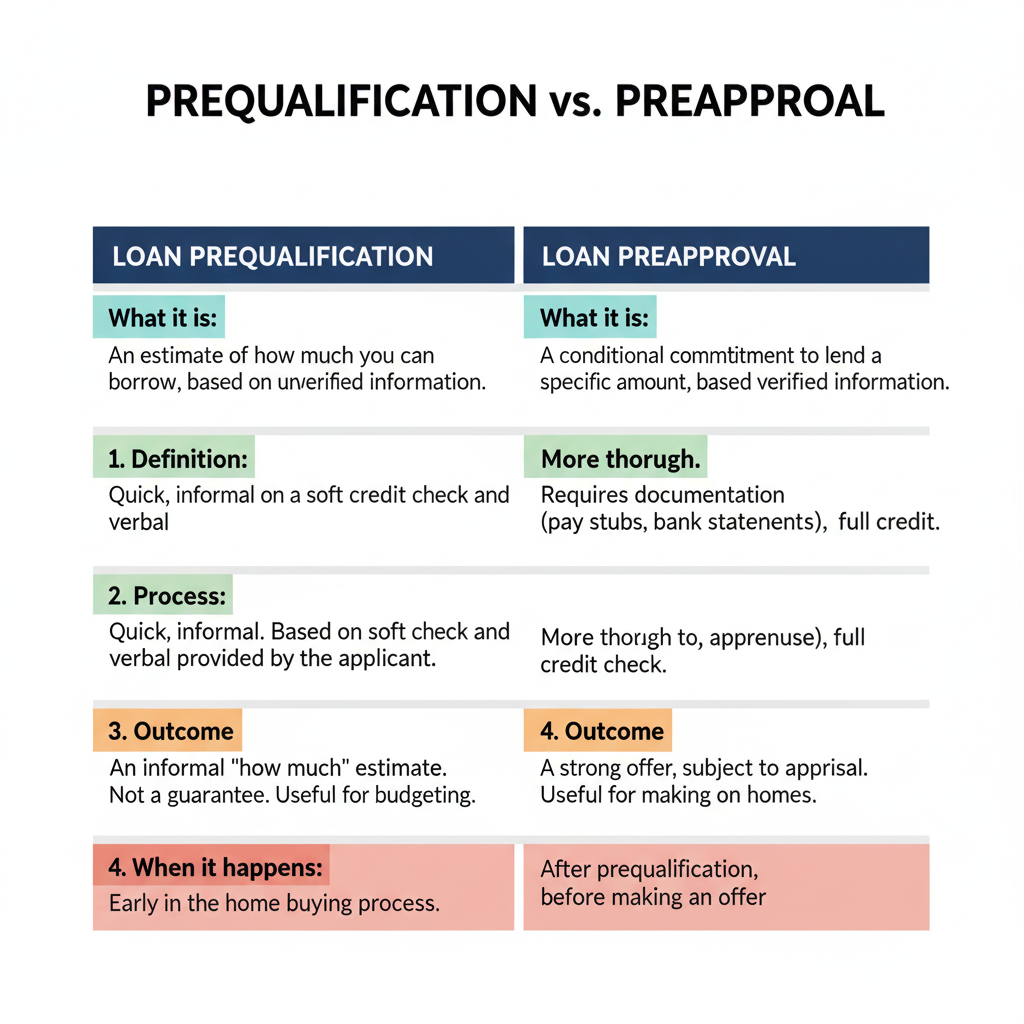

Pre‑Qualification vs Pre‑Approval: What's the Real Difference?

Many homebuyers confuse these terms, but understanding the distinction could mean the difference between your offer being accepted or rejected in a competitive market.

Pre‑qualification is essentially an estimate based on self‑reported information. It's quick, usually done online or over the phone, and doesn't involve a deep dive into your finances. It's a good first step to ballpark what you might afford, but it's not binding and doesn't carry much weight with sellers.

Pre‑approval, on the other hand, means a lender has actually reviewed your documents—income, assets, debts, and credit—and issued a conditional commitment for a specific loan amount. This process involves a hard credit check and thorough verification. Sellers take pre‑approval seriously because it signals you're a prepared, serious buyer who can actually secure financing.

In today's competitive markets, many real estate agents won't even show homes to buyers without a pre-approval letter. It's that important.

Pre‑approval checklist: What you'll need

Gathering these documents ahead of time will make the process smoother:

- Proof of income (recent pay stubs, W‑2s/1099s from the past two years, tax returns)

- Bank and asset statements for the last 2–3 months (checking, savings, investment accounts)

- Government ID & proof of residency

- Employment verification or business financials (if you're self‑employed)

- Credit report authorization

- List of debts (auto loans, student loans, credit cards)

- Explanation for any large deposits (lenders want to ensure the money is legitimately yours)

Once you're pre‑approved, it's crucial to stay "credit quiet": avoid opening new lines of credit, making large purchases, or changing jobs until after closing. Even something as innocent as buying new appliances on credit before closing could jeopardize your loan approval.

The Pre-Approval Timeline: What to Expect

The pre-approval process typically takes 1-3 business days once you've submitted all required documentation. During this time, the lender's underwriters will:

- Verify your employment and income

- Review your credit history and score

- Analyze your debt-to-income ratios

- Assess your assets and reserves

- Evaluate the overall risk of lending to you

If everything checks out, you'll receive a pre-approval letter stating the maximum loan amount you qualify for. This letter is typically valid for 60-90 days, after which you'll need to update your financial information if you haven't found a home yet.

Remember: pre-approval isn't a guarantee of final loan approval. The property itself must also meet the lender's standards through appraisal and inspection. But it's the strongest position from which to begin your home search.

Rates, Terms & Types of Mortgages: Finding Your Fit

Your mortgage type shapes your risk and total cost. Here are the big buckets, with more detail than you'll find in most guides.

Fixed‑rate mortgages (FRM)

With a fixed-rate mortgage, your interest rate stays the same for the entire term (typically 15, 20, or 30 years). This predictability makes budgeting easier, as your principal and interest payment never changes. A 15‑year FRM can save tens of thousands in interest but has significantly higher monthly payments. Many buyers opt for a 30-year term for the lower payments, then make extra principal payments when possible to simulate a shorter loan term.

Fixed-rate mortgages are ideal when:

- You plan to stay in the home long-term (10+ years)

- Interest rates are historically low

- You prefer payment stability over potential savings

- Your budget is tight and you need predictable payments

Adjustable‑rate mortgages (ARM)

ARMs start with a fixed period (common terms are 5/1, 7/1, or 10/1, where the first number is the fixed years and the second is how often it adjusts after that), then adjust periodically based on an index plus a margin, within predetermined caps. ARMs can be cheaper initially but may rise later. They're suitable if you plan to sell or refinance before adjustments begin.

Understanding ARM caps is crucial:

- Initial cap: How much the rate can increase after the fixed period ends

- Periodic cap: How much the rate can change at each adjustment period

- Lifetime cap: The maximum rate increase over the life of the loan

ARMs make sense when:

- You plan to move before the fixed period ends

- You expect your income to increase significantly

- Interest rates are high and expected to fall

- You can handle potential payment increases

Other mortgage variations

- Interest‑only: Lower initial payments, but principal doesn't drop during the interest‑only phase (typically 5-10 years). After that, payments jump significantly as you begin paying principal.

- Balloon: Small payments now, a big balance later—risky unless you have a clear exit plan. These are less common now than in the past.

- Government‑backed: FHA/VA/USDA programs help with lower down payments or unique eligibility:

- FHA loans: Require as little as 3.5% down but include upfront and annual mortgage insurance

- VA loans: For veterans and active military, offering 0% down with no PMI

- USDA loans: For rural properties, offering 0% down with income restrictions

| Loan Type | Down Payment | Best For | Considerations |

|---|---|---|---|

| Conventional 30-year fixed | 3-20% | Long-term homeowners, stability seekers | PMI if down payment < 20% |

| Conventional 15-year fixed | 5-20% | Rapid equity building, lower interest costs | Higher monthly payments |

| 5/1 ARM | 3-20% | Short-term owners, expect to move in 5-7 years | Rate can increase after 5 years |

| FHA loan | 3.5% | First-time buyers, lower credit scores | Upfront and annual mortgage insurance |

| VA loan | 0% | Veterans, active military | Funding fee, specific eligibility |

How to Choose: A Practical Framework

With all these options, how do you decide? Ask yourself these questions:

- How long do I plan to stay in this home? If less than 7 years, an ARM might save you money. If longer, a fixed rate provides stability.

- How would I handle payment increases? If a significant payment hike would strain your budget, stick with a fixed rate.

- What's my risk tolerance? If market fluctuations and payment changes would keep you up at night, a fixed rate is worth the potential premium.

- What are my future income prospects? If you expect significant raises or career advancement, you might comfortably handle potential ARM adjustments.

There's no one-size-fits-all answer. The right mortgage depends on your personal circumstances, goals, and comfort with risk.

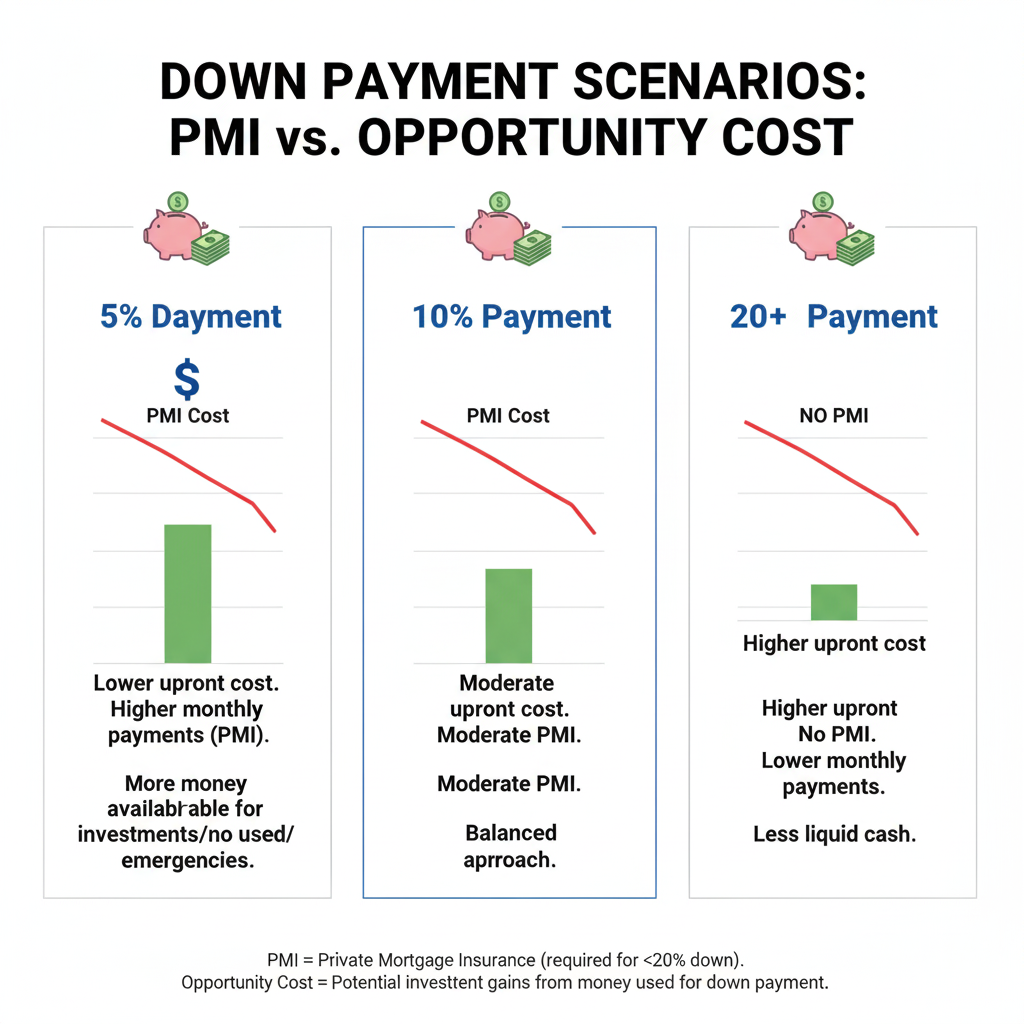

Down Payment, PMI & Loan‑to‑Value (LTV): The 20% Myth

Your down payment affects LTV (loan divided by home value). Higher down payments reduce risk and may eliminate private mortgage insurance (PMI) on conventional loans. But don't drain your emergency fund—owning a home comes with surprise expenses.

The traditional advice has always been "put 20% down to avoid PMI." While this is financially efficient, it's not always practical—especially for first-time buyers in expensive markets. Let's break down the realities.

Finding the balance

- Below 20% down: Expect PMI until you reach 80% LTV (or sometimes automatic removal at 78%). PMI typically costs 0.5-1% of the loan amount annually, divided into monthly payments.

- 20% down: Often no PMI, stronger offers, lower monthly payment. This is the sweet spot for conventional loans.

- More than 20%: Smaller loan, less interest—but consider opportunity cost if you have higher‑yield uses for cash. There's rarely a financial benefit to putting down more than 20% unless you're negotiating a lower rate.

Use the Saving Goal Calculator to plan your down payment timeline and the Mortgage Calculator to compare scenarios with and without PMI.

The PMI Details Many Miss

Private Mortgage Insurance isn't forever, and it's not as scary as many think. Here's what you need to know:

- Automatic termination: For conventional loans, PMI automatically drops off when you reach 78% LTV based on the original amortization schedule.

- Early termination: You can request PMI removal when you reach 80% LTV, but you may need a new appraisal to prove your home's value hasn't declined.

- FHA loans: Mortgage insurance works differently—it's for the life of the loan if you put down less than 10%. With 10% or more down, it drops off after 11 years.

- Lender-paid PMI: Some lenders offer to pay your PMI in exchange for a slightly higher interest rate. Run the numbers to see if this makes sense for your situation.

The Opportunity Cost Consideration

While avoiding PMI is desirable, consider what else you could do with that money:

- Investing in retirement accounts with potential market returns

- Paying down higher-interest debt

- Building a robust emergency fund (especially important as a homeowner)

- Funding home improvements that increase property value

Sometimes, putting less down and paying PMI temporarily is the smarter financial move—especially if it allows you to buy sooner in a rising market or avoid draining your reserves.

Creative Down Payment Strategies

If you're struggling to save a down payment, consider these approaches:

- Gift funds: Family members can gift money for your down payment, with proper documentation.

- Down payment assistance programs: Many states and municipalities offer grants or low-interest loans for first-time buyers.

- 401(k) loan: You can borrow from your 401(k) for a down payment, though this comes with risks if you lose your job.

- Side hustles: Dedicate extra income specifically to your down payment fund.

- Automated savings: Set up automatic transfers to a dedicated savings account each pay period.

Remember: your down payment is just one piece of the homebuying puzzle. A slightly smaller down payment might get you into a home sooner, building equity rather than paying rent.

More Reading on Proculator

Level up your money and math skills with these related resources: