Albert Einstein famously called compound interest "the eighth wonder of the world," adding that "he who understands it, earns it; he who doesn't, pays it." This powerful financial concept has created countless fortunes over centuries, yet remains misunderstood or underutilized by many.

At its core, compound interest is simply interest earning interest on itself—a snowball effect that can transform modest savings into substantial wealth over time. Whether you're saving for retirement, a child's education, or financial independence, understanding compound interest is essential for making your money work harder for you.

In this comprehensive guide, we'll explore the mathematics, history, and practical applications of compound interest. You'll learn how to calculate it, how to maximize its benefits, and how to avoid its pitfalls when you're on the borrowing side of the equation.

What Exactly is Compound Interest?

Compound interest is the interest calculated on the initial principal and also on the accumulated interest of previous periods. This differs from simple interest, where interest is calculated only on the principal amount.

Think of it as a financial feedback loop where your earnings generate more earnings. This creates exponential growth over time, which is why compound interest is so powerful for long-term wealth building.

A Simple Example

Imagine you invest $1,000 at a 10% annual interest rate:

- Year 1: $1,000 × 10% = $100 in interest → New balance: $1,100

- Year 2: $1,100 × 10% = $110 in interest → New balance: $1,210

- Year 3: $1,210 × 10% = $121 in interest → New balance: $1,331

With simple interest, you would have earned exactly $100 each year ($1,000 × 10%), ending with $1,300 after three years. With compound interest, you earned $331—$31 more than simple interest would have generated. This difference seems small at first but becomes enormous over longer periods.

Key Insight: The power of compound interest doesn't come from high returns or large investments—it comes from time. The longer your money compounds, the more dramatic the growth becomes.

The Compound Interest Formula Explained

While you can use our Compound Interest Calculator to do the math for you, understanding the formula helps you appreciate exactly how the variables interact.

The standard compound interest formula is:

Where:

- A = the future value of the investment/loan, including interest

- P = the principal investment amount (the initial deposit or loan amount)

- r = the annual interest rate (decimal)

- n = the number of times that interest is compounded per year

- t = the number of years the money is invested or borrowed for

Breaking Down the Components

Let's examine each part of the formula:

Principal (P): This is your starting amount. While increasing your principal obviously increases your returns, the real power comes from time and compounding frequency.

Interest Rate (r): Expressed as a decimal (so 5% becomes 0.05). Small differences in rates can create significant differences over long periods. For example, the difference between 7% and 8% annual returns might seem small, but over 30 years, that 1% difference can result in hundreds of thousands of dollars in additional growth on a substantial investment.

Compounding Frequency (n): How often interest is calculated and added to your principal. Common compounding frequencies include:

- Annually (1 time per year)

- Semi-annually (2 times per year)

- Quarterly (4 times per year)

- Monthly (12 times per year)

- Daily (365 times per year)

The more frequently interest compounds, the faster your money grows. For example, $10,000 invested at 5% interest for 10 years would grow to:

- $16,288.95 with annual compounding

- $16,386.16 with quarterly compounding

- $16,470.09 with monthly compounding

Time (t): The most powerful variable in the equation. Doubling your time more than doubles your result due to exponential growth. This is why starting early is so crucial for investors.

Pro Tip: The formula (1 + r/n)^(nt) is known as the "compound factor." It shows how many times your money will multiply at a given rate over a specific period. Understanding this helps you set realistic expectations for your investments.

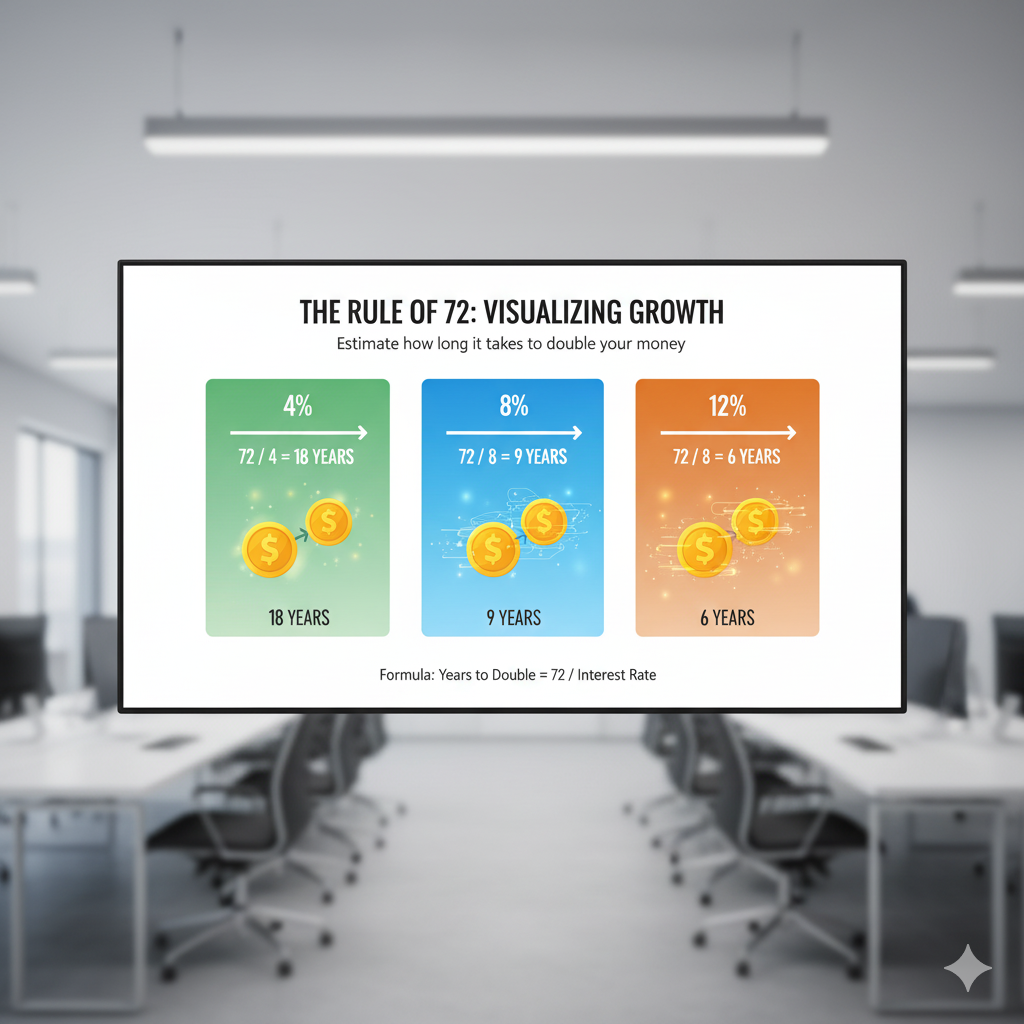

The Rule of 72: Quick Doubling Estimates

The Rule of 72 is a simple mental shortcut to estimate how long an investment will take to double, given a fixed annual rate of interest. You simply divide 72 by the annual rate of return.

Examples:

- At 6% return, your money doubles in 72 ÷ 6 = 12 years

- At 8% return, your money doubles in 72 ÷ 8 = 9 years

- At 12% return, your money doubles in 72 ÷ 12 = 6 years

You can also use the rule to determine what interest rate you'd need to double your money in a specific time frame:

Examples:

- To double money in 8 years: 72 ÷ 8 = 9% return needed

- To double money in 15 years: 72 ÷ 15 = 4.8% return needed

Limitation: The Rule of 72 is most accurate for interest rates between 6% and 10%. For rates outside this range, the rule becomes less precise but still provides a reasonable estimate. For higher accuracy, especially with very high or very low rates, using the actual compound interest formula is better.

The Rule of 72 demonstrates why small differences in returns matter significantly over time. A 2% difference in annual return might seem small, but it can shave years off the time needed to reach your financial goals. For instance, at 6% returns, your money doubles every 12 years, but at 8% returns, it doubles every 9 years. That 2% difference means your money will double three times in 27 years at 8%, compared to just twice in 24 years at 6%.

Key Factors That Affect Compound Interest

Several variables influence how quickly your money grows through compounding. Understanding these can help you maximize your returns:

1. Time Horizon

This is the most critical factor. The longer your money compounds, the more dramatic the growth. Starting early provides a tremendous advantage that's difficult to overcome later. Consider this: if you invest $5,000 annually from age 25 to 35 (10 years) and then stop, you'll likely end up with more money at retirement than someone who starts at 35 and invests $5,000 annually until 65 (30 years).

2. Interest Rate

Higher rates accelerate growth, but it's important to balance return with risk. Consistently reasonable returns often outperform volatile high returns. A portfolio that grows steadily at 7% annually will often outperform one that alternates between 15% gains and 5% losses unpredictably.

3. Compounding Frequency

More frequent compounding leads to faster growth. Daily compounding generates slightly more return than monthly, which generates more than quarterly, and so on. While the differences may seem small initially, over decades, they can add up to significant amounts.

4. Regular Contributions

Adding money regularly (dollar-cost averaging) can significantly boost your ending balance. Even small monthly contributions add up substantially over decades. For example, adding just $100 monthly to an investment earning 7% annually would grow to over $100,000 in 25 years.

5. Taxes

Taxes can significantly erode compounding benefits. Tax-advantaged accounts like IRAs, 401(k)s, or 529 plans help preserve more of your returns for compounding. The difference between taxable and tax-advantaged investing can amount to hundreds of thousands of dollars over an investing lifetime.

6. Inflation

Inflation reduces purchasing power. Your real return is your nominal return minus inflation. Aim for returns that outpace inflation to build real wealth. Historically, inflation has averaged about 3% annually, so you need returns above this to actually grow your purchasing power.

Historical Context: Over the past century, the U.S. stock market has returned about 10% annually before inflation and 7% after inflation. This long-term average demonstrates the real wealth-building potential of equities. However, it's important to remember that past performance doesn't guarantee future results, and these returns came with significant volatility along the way.

Real-World Examples of Compound Interest

Let's examine how compound interest works in various scenarios:

Example 1: Retirement Savings

Sarah starts investing $5,000 annually at age 25. She earns 7% annually and stops contributing at age 35, having invested $50,000 total. By age 65, her investment grows to approximately $602,000.

John waits until age 35 to start investing but contributes $5,000 annually until age 65. He invests $150,000 total—three times more than Sarah. At the same 7% return, his investment grows to approximately $540,000—less than Sarah's despite contributing more money.

This demonstrates the incredible power of starting early. Sarah's money had more time to compound, which more than made up for her smaller total contributions. The extra 10 years of compounding made a difference of over $60,000, even though she contributed $100,000 less than John.

Example 2: Credit Card Debt

Compound interest works against you when you borrow. Suppose you have a $5,000 credit card balance at 18% APR. If you make only minimum payments (typically 2-3% of balance), it could take over 30 years to pay off and cost more than $10,000 in interest.

This example shows why high-interest debt is so dangerous. The compounding effect that helps investors build wealth can trap borrowers in cycles of debt that are difficult to escape. This is why financial advisors typically recommend paying off high-interest debt before focusing on investments.

Example 3: Education Savings

If you save $200 monthly for a child's education from birth to age 18 at 7% return, you'll contribute $43,200 but accumulate approximately $85,000. The compound interest generates nearly as much as your contributions.

This example demonstrates how consistent contributions combined with compound interest can help you reach significant financial goals. The $200 monthly might seem manageable for many families, but the result after 18 years is a substantial education fund that could cover a significant portion of college expenses.

Comparison of Starting Ages for Retirement Savings

Starting at 25 vs. 35 with $5,000 annual contributions at 7% return

Strategies to Maximize Compound Interest

Now that you understand compound interest, here's how to make it work most effectively for you:

1. Start Early

Time is your greatest ally. Even small amounts invested early can outperform larger amounts invested later. Don't wait until you have "enough" to start—begin with what you can. If you're in your 20s or 30s, recognize that your greatest investing advantage is the decades of compounding ahead of you.

2. Be Consistent

Regular contributions harness the power of dollar-cost averaging and ensure you're continuously adding fuel to the compounding fire. Set up automatic contributions to make investing a habit rather than something you do sporadically.

3. Reinvest Dividends and Interest

Always choose to reinvest earnings rather than taking them as cash. This automatically compounds your returns. Many investment platforms offer automatic dividend reinvestment plans (DRIPs) that make this process seamless.

4. Minimize Fees

Investment fees directly reduce your compounding rate. A 1% annual fee might seem small, but over decades it can reduce your ending balance by 25% or more. Choose low-cost index funds and ETFs whenever possible.

5. Avoid Withdrawals

Every withdrawal interrupts compounding and reduces your principal. Let your investments grow undisturbed whenever possible. Create a separate emergency fund so you don't need to tap your investments for unexpected expenses.

6. Use Tax-Advantaged Accounts

IRAs, 401(k)s, HSAs, and 529 plans allow your money to grow either tax-free or tax-deferred, preserving more for compounding. Maximize contributions to these accounts before investing in taxable brokerage accounts.

7. Increase Contributions Over Time

As your income grows, increase your contribution percentage. This accelerates compounding without significantly impacting your lifestyle. Consider dedicating a portion of any raise or bonus to your investments.

8. Stay Invested During Market Downturns

It can be tempting to sell during market crashes, but staying invested allows you to benefit from the eventual recovery. Historically, markets have always recovered from downturns and gone on to reach new highs.

Wealth-Building Insight: The perfect investment strategy is less about picking superstar stocks and more about consistent contributions, patience, and letting compound interest work its magic over decades. The most successful investors are often those who simply stay the course through market ups and downs.

The Historical Context of Compound Interest

Compound interest isn't a modern invention. Its principles have been understood for millennia:

Ancient Understanding

Clay tablets from ancient Mesopotamia (around 2400 BCE) show evidence of compound interest calculations. The Code of Hammurabi (1754 BCE) actually regulated interest rates on loans, indicating that the concept of interest was well-established in ancient economies.

Renaissance Mathematics

Italian mathematician Luca Pacioli, in his 1494 work "Summa de arithmetica," described the Rule of 72, though the rule likely predates his writing. This suggests that merchants and bankers of the time had a practical understanding of compound interest even if they didn't express it in modern mathematical terms.

Modern Applications

In the 20th century, compound interest became foundational to retirement planning and long-term investing strategies. The creation of tax-advantaged retirement accounts made compounding accessible to millions of ordinary people rather than just the wealthy.

The development of modern portfolio theory in the 1950s and the rise of index investing in the 1970s provided practical tools for investors to harness compound interest through diversified, low-cost investments.

Historical Note: Albert Einstein likely never actually called compound interest the "eighth wonder of the world," but the attribution persists because it perfectly captures the concept's power. The quote appears to have been invented by financial writers in the late 20th century, but it remains popular because it succinctly expresses the transformative potential of compound interest.

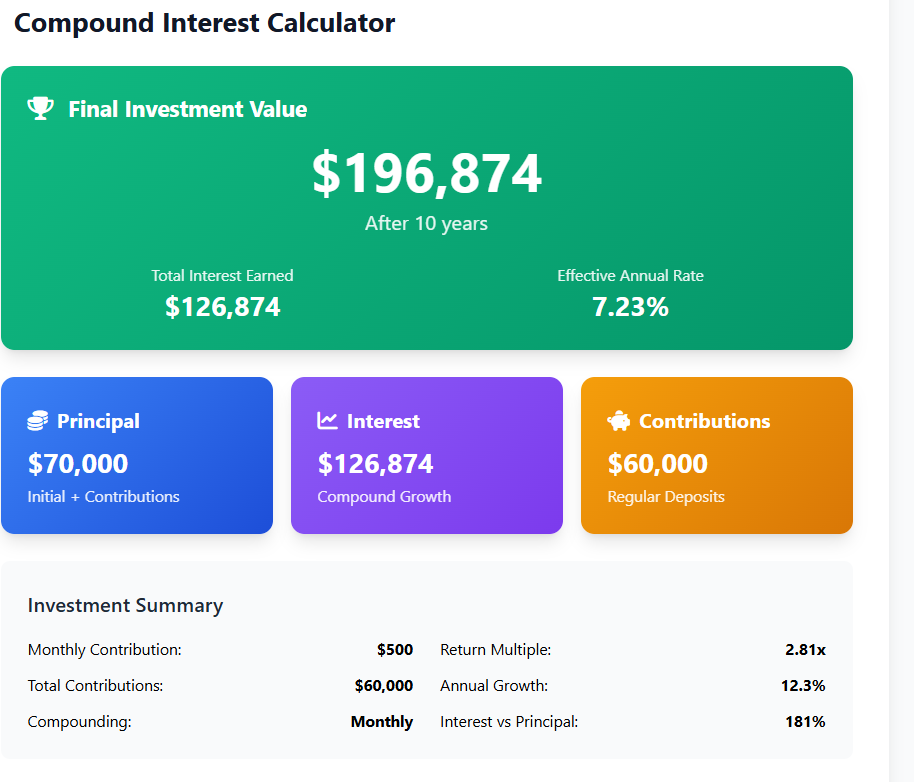

How to Use Compound Interest Calculators

While understanding the formula is valuable, our Compound Interest Calculator makes the process simple and visual. Here's how to use it effectively:

Step 1: Enter Your Initial Investment

This is your principal—the amount you're starting with. If you're starting from zero, that's okay too. Many successful investors began with small amounts and added to them regularly over time.

Step 2: Add Regular Contributions

Input how much you plan to add regularly and how often (monthly, quarterly, etc.). Consistent contributions significantly boost your results. Even small amounts added regularly can make a big difference over time.

Step 3: Set Your Interest Rate

Use a realistic rate based on historical returns for your investment type. For long-term stock market investments, 7-10% before inflation is reasonable. For more conservative investments, use lower rates like 3-5%.

Step 4: Choose Compounding Frequency

Select how often interest compounds. For most investments, this is daily or monthly. The calculator will show you how small differences in compounding frequency affect your results over long periods.

Step 5: Set Your Time Horizon

Input how long you plan to let your money grow. Remember, time is your most powerful variable. Even extending your time horizon by a few years can significantly impact your results.

Step 6: Calculate and Analyze

Review the results, including your ending balance, total contributions, and interest earned. The visual graph helps you understand the growth trajectory and how compounding accelerates over time.

Pro Tip: Use the calculator to run different scenarios. What happens if you increase contributions by 1% annually? What if you start five years earlier? These experiments reveal the most impactful variables for your situation. Try adjusting each variable one at a time to see which has the greatest effect on your results.

Frequently Asked Questions About Compound Interest

How often should interest compound for maximum growth?

Daily compounding provides the maximum mathematical benefit, but the difference between daily and monthly compounding is relatively small. More important than compounding frequency is finding investments with good long-term returns and keeping fees low. The difference between 7% and 8% annual returns is far more significant than the difference between monthly and daily compounding at the same rate.

Can compound interest make me rich quickly?

Compound interest is a wealth-building strategy, not a get-rich-quick scheme. Its power emerges over decades, not years. Patience and consistency are key. While stories of rapid wealth creation through investments like Bitcoin capture attention, most sustainable wealth is built gradually through consistent investing and compounding over long periods.

How does inflation affect compound interest?

Inflation reduces the purchasing power of your returns. Your real return is your nominal return minus inflation. Historically, stocks have returned about 7% after inflation, bonds about 2-3%. This is why it's important to focus on real returns rather than nominal returns when planning for long-term goals like retirement.

Is compound interest available on savings accounts?

Yes, most savings accounts compound interest daily or monthly. However, interest rates on savings accounts are typically lower than investment returns, so they're better for emergency funds than long-term wealth building. Online banks often offer higher rates than traditional brick-and-mortar banks.

How can I benefit from compound interest if I'm starting late?

While starting early is ideal, it's never too late to benefit from compound interest. Focus on increasing your contribution rate and consider slightly more aggressive investments (within your risk tolerance). Also, plan to work slightly longer to give your money more time to compound. Remember that even 10-15 years of compounding can still significantly grow your investments.

Does compound interest work the same way with debt?

Yes, compound interest works against you when you have debt, especially high-interest debt like credit cards. The same exponential growth that helps investments grow works against you with debt, causing balances to balloon if only minimum payments are made. This is why paying off high-interest debt should typically be a priority before investing.

How does compound interest affect retirement planning?

Compound interest is the foundation of retirement planning. It allows relatively small regular contributions to grow into substantial sums over a working career. The longer your time horizon until retirement, the more powerful compounding becomes. This is why starting retirement savings early is so strongly emphasized by financial advisors.

Ready to See Your Wealth Grow?

Use our Compound Interest Calculator to project your financial future and create a personalized wealth-building strategy.

Calculate Your Compound InterestConclusion: Harnessing the Most Powerful Force in Finance

Compound interest is indeed the closest thing to magic in the financial world. It transforms regular savings into substantial wealth, turns time into your greatest ally, and provides a mathematical path to financial security.

The principles we've explored are simple but profound: start early, contribute consistently, reinvest earnings, minimize costs, and be patient. While these steps aren't flashy or complicated, their long-term impact is extraordinary.

Remember that compound interest works both ways—it can build wealth when you're investing, but it can create debt traps when you're borrowing. Be mindful of high-interest debt, which compounds against you just as aggressively as investments compound for you.

At Proculator, we're committed to providing the tools and knowledge you need to make compound interest work for you. Whether you're just starting your financial journey or looking to optimize existing investments, understanding this concept is fundamental to achieving your goals.

The best time to start harnessing compound interest was yesterday. The second-best time is today. Even small steps taken now can create a dramatically different financial future. Open that retirement account, set up automatic contributions, and watch as time and compound interest work together to build your wealth.