The Ultimate Loan Guide — How to Calculate, Plan & Repay Loans Effectively

A complete, practical guide from Proculator to help you understand different types of loans, how interest and EMIs work, and how to use calculators to plan your borrowing and repayment strategy.

Why a Loan Guide Matters

Borrowing money is one of the most common financial actions people undertake — from short-term personal loans to long-term mortgages. Yet many borrowers underestimate how much interest they will pay over time or which repayment options will save them money. This guide breaks down loan fundamentals into plain language and links you to Proculator tools so you can practise calculations and make data-driven decisions.

According to recent studies, the average American household carries approximately $101,915 in debt, including mortgages, credit cards, auto loans, and student loans. With such significant financial commitments, understanding how loans work isn't just helpful—it's essential for your financial health.

This comprehensive guide will walk you through everything from basic loan terminology to advanced repayment strategies. Whether you're considering your first loan or looking to optimize existing debt, you'll find practical advice and tools to make informed decisions.

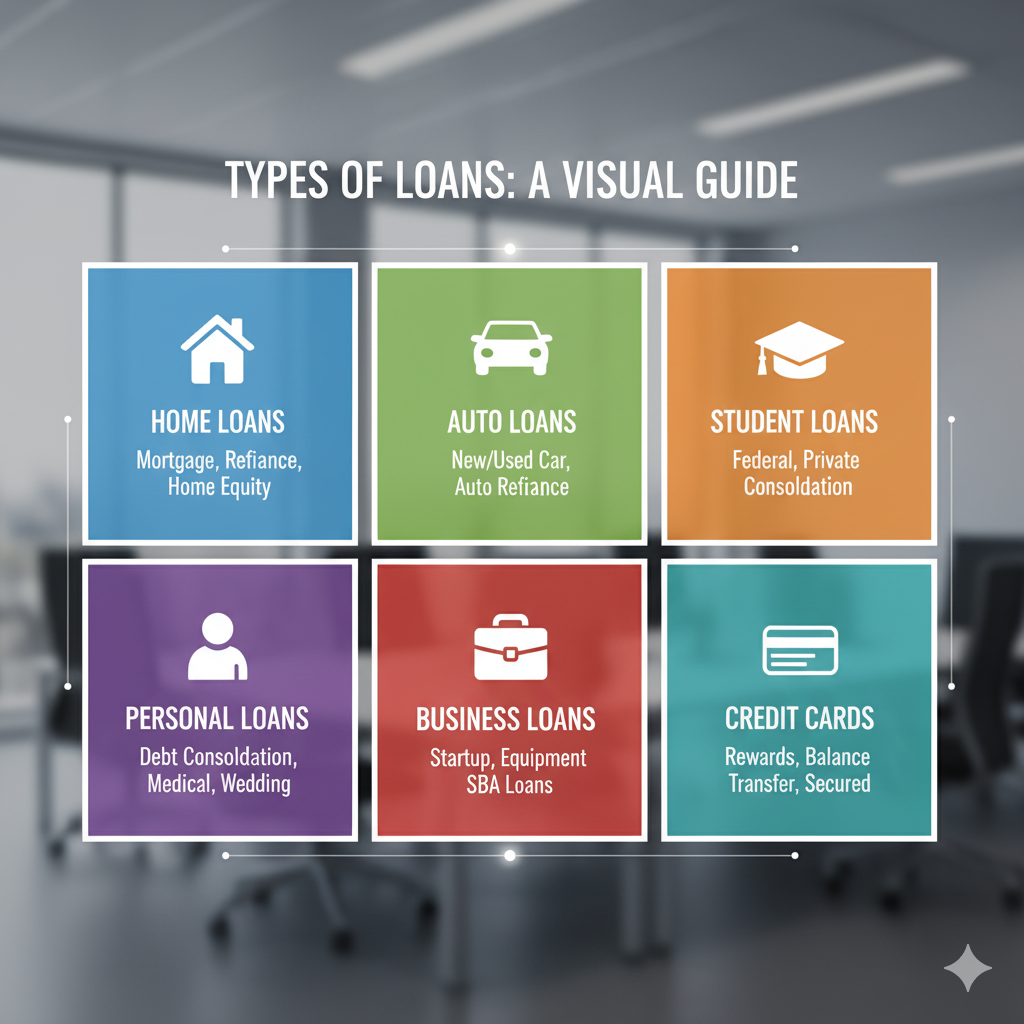

Common Types of Loans

Understanding loan types helps you pick the right product and the right calculator. Below are the most common loan categories:

- Personal loans — unsecured loans for general purposes such as medical bills or debt consolidation. These typically have higher interest rates than secured loans since the lender assumes more risk. Terms usually range from 1-7 years with amounts from $1,000 to $100,000.

- Home loans / Mortgages — long-term secured loans for buying property. Use our Mortgage Calculator and Home Loan Prepayment Calculator to model scenarios. These loans typically span 15-30 years and offer lower interest rates since the property serves as collateral.

- Auto loans — vehicle financing, often with fixed rates and terms. These are secured by the vehicle itself, which means the lender can repossess the car if you default. Terms typically range from 3-7 years.

- Student loans — education financing programs with special repayment or deferment options. See our Student Calculator Guide for related planning tips. These often have lower interest rates and flexible repayment options but are difficult to discharge in bankruptcy.

- Business loans — financing for small or large business needs; may require collateral or business plans. These can be used for startup costs, expansion, equipment purchases, or working capital.

- Payday loans — short-term, high-cost loans typically due on your next payday. These should be avoided whenever possible due to extremely high APRs that can exceed 400%.

Warning: Payday loans and car title loans often trap borrowers in cycles of debt due to extremely high interest rates and fees. Explore all other options before considering these loan types.

Interest Rates: Fixed vs Floating

Interest is the cost of borrowing. Two main rate structures appear in loan contracts:

- Fixed rate — remains constant for the life of the loan. Predictable monthly payments help budgeting. This is ideal when interest rates are low and expected to rise. You'll pay slightly more initially for this stability, but it protects you from future rate increases.

- Floating (variable) rate — tied to a benchmark (e.g., prime rate). Payments vary with market rates and may be lower initially but can increase later. These often start with lower rates than fixed loans but carry the risk of payment increases if interest rates rise.

Pro tip: use the Loan Calculator to compare the total interest paid under fixed and variable rate examples by entering hypothetical rates.

How Interest Rates Are Determined

Lenders determine your interest rate based on several factors:

- Credit score: Higher scores typically qualify for lower rates

- Loan term: Shorter terms often have lower rates

- Loan amount: Larger loans might qualify for better rates

- Debt-to-income ratio: Lower ratios demonstrate better ability to repay

- Economic conditions: Broader economic factors affect all rates

- Loan type: Secured loans typically have lower rates than unsecured

Even a small difference in your interest rate can save you thousands over the life of a loan. For example, on a $300,000 30-year mortgage, the difference between 4% and 4.5% is over $30,000 in additional interest payments.

What is EMI & How to Calculate It

EMI (Equated Monthly Installment) is the fixed monthly payment that repays both principal and interest. The standard formula for EMI is:

EMI = P * r * (1 + r)^n / ((1 + r)^n - 1)Where:

P = principal loan amount

r = monthly interest rate (annual rate / 12)

n = number of monthly payments (loan term in months)

Instead of doing this manually, try our Loan Calculator or the Mortgage Calculator to instantly compute EMI and see amortization schedules.

Understanding Your Amortization Schedule

An amortization schedule shows the breakdown of each payment into principal and interest components. In the early years of a loan, most of your payment goes toward interest rather than principal. As time passes, this ratio gradually shifts.

Here's a simplified example of how an amortization schedule works for a $200,000 loan at 4% interest for 30 years:

| Year | Total Payment | Principal Paid | Interest Paid | Remaining Balance |

|---|---|---|---|---|

| 1 | $11,528 | $3,528 | $8,000 | $196,472 |

| 5 | $11,528 | $4,212 | $7,316 | $179,674 |

| 10 | $11,528 | $5,225 | $6,303 | $148,679 |

| 20 | $11,528 | $7,729 | $3,799 | $72,852 |

| 30 | $11,528 | $11,528 | $0 | $0 |

As you can see, in the first year, nearly 70% of your payment goes toward interest. By year 20, this ratio has flipped, with most of your payment reducing the principal. This is why making extra payments early in the loan term has such a powerful impact on reducing total interest paid.

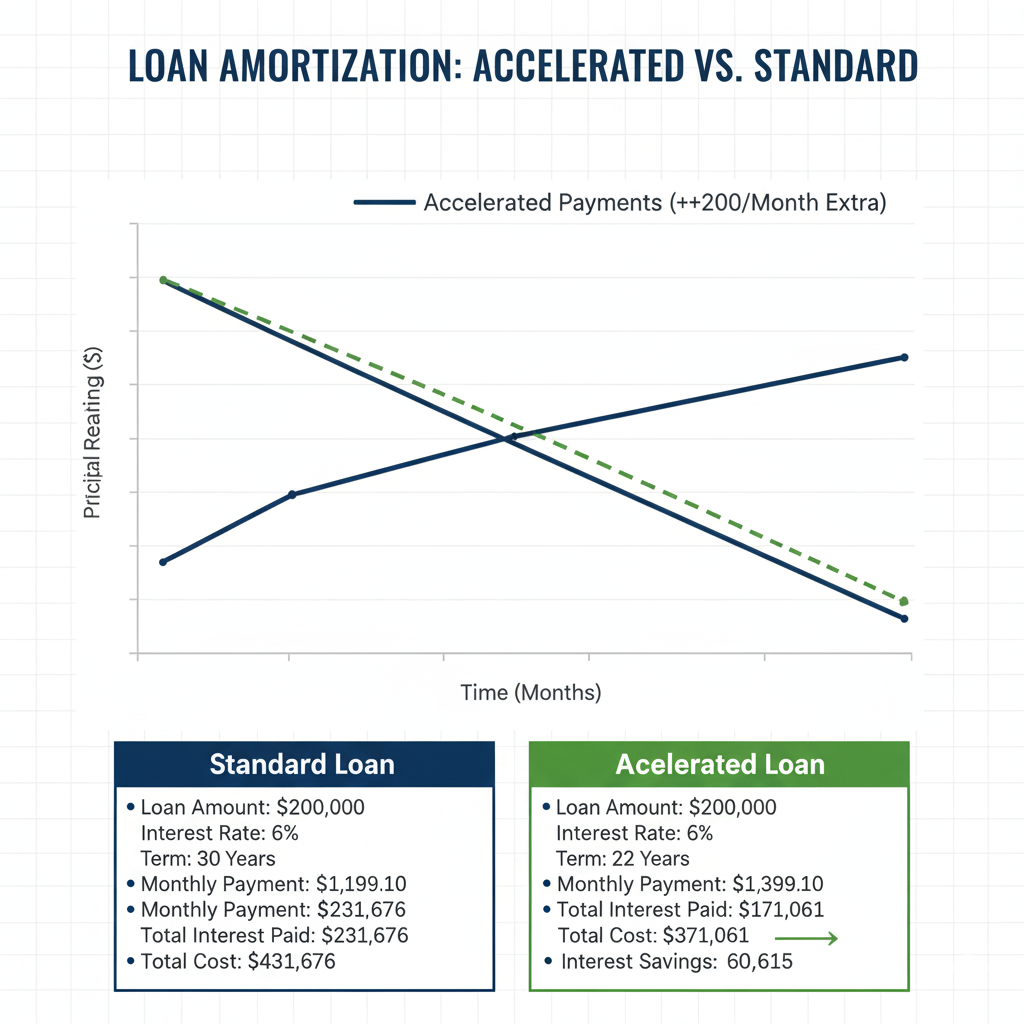

Amortization & Why Early Payments Help

An amortization schedule shows how each EMI is split between interest and principal. Early payments mostly cover interest; as principal reduces, a greater portion of later payments goes to principal. When you make extra payments (prepayments), you cut the outstanding principal early, which reduces future interest and often shortens the loan term.

You can model extra payments using our Home Loan Prepayment Calculator to see how much interest you save and how many months you shave off your loan.

The Power of Small Additional Payments

Even modest additional payments can have a dramatic impact on your loan. Let's consider a $250,000 mortgage at 4% interest for 30 years:

- Without extra payments: Total interest = $179,674

- With $100 extra monthly: Total interest = $147,188 (saving $32,486)

- Loan term reduced by 4 years and 8 months

- With $200 extra monthly: Total interest = $126,704 (saving $52,970)

- Loan term reduced by 7 years and 2 months

As you can see, even relatively small additional payments can save tens of thousands of dollars and reduce your loan term by several years.

Pro Tip: When making extra payments, specify that they should be applied to principal reduction. Some lenders might apply extra payments to future installments instead, which doesn't provide the same interest-saving benefits.

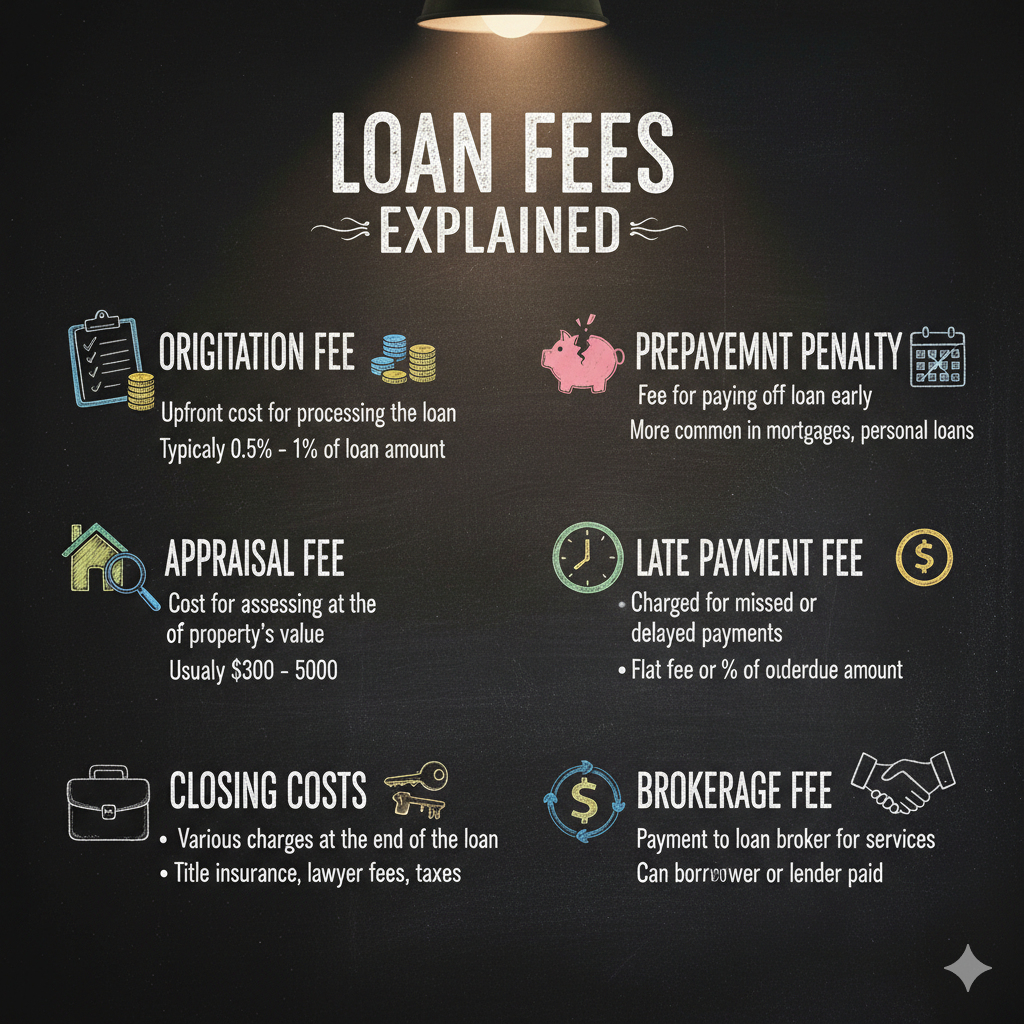

Loan Fees & Total Cost

The true cost of a loan includes fees: origination fees, processing fees, prepayment penalties, late fees, and insurance. Always calculate the total cost (principal + total interest + fees) and compare loan offers using the Annual Percentage Rate (APR), which standardizes the cost across lenders.

Our Compound Interest Calculator and Saving Goal Calculator can help you plan for fees and savings needed for downpayments or emergency buffers.

Common Loan Fees to Watch For

| Fee Type | Typical Cost | Description |

|---|---|---|

| Origination Fee | 0.5% - 1% of loan amount | Charged for processing the loan application |

| Application Fee | $25 - $50 | Non-refundable fee to process your application |

| Prepayment Penalty | 2-5% of prepaid amount | Fee for paying off loan early (avoid loans with this) |

| Late Payment Fee | $15 - $35 or 3-5% of payment | Charged when payments are received after due date |

| Annual Fee | $25 - $100 | Some personal loans charge annual maintenance fees |

When comparing loans, always look at the APR (Annual Percentage Rate) rather than just the interest rate. The APR includes both interest and certain fees, giving you a more accurate picture of the total cost of borrowing.

Practical Strategies to Save on Loans

- Shop multiple lenders — compare rates and APRs; small rate differences compound over long terms. Get quotes from at least 3-5 lenders before deciding.

- Make extra payments when possible — even modest additional monthly payments can cut years off a mortgage. Consider using windfalls like tax refunds or bonuses for lump-sum payments.

- Refinance wisely — when rates drop significantly, refinancing can lower monthly payments or shorten the term, but account for closing costs. Calculate the break-even point to ensure refinancing makes financial sense.

- Prioritize high-interest debt — pay down credit cards and high-rate personal loans first. Consider the debt avalanche method (paying highest interest rates first) for maximum interest savings.

- Use calculators — Proculator tools like SIP Calculator or Salary After Tax Calculator help with realistic budgeting.

- Consider bi-weekly payments — making half-payments every two weeks results in 26 half-payments or 13 full payments per year, effectively making one extra payment annually.

- Improve your credit score before applying — a higher credit score can qualify you for significantly better interest rates, saving thousands over the loan term.

The Debt Snowball vs. Debt Avalanche Methods

When dealing with multiple debts, two popular strategies can help you become debt-free faster:

Debt Snowball Method: Pay minimums on all debts, but put extra money toward the smallest debt first. Once that's paid off, move to the next smallest. This method provides psychological wins that keep you motivated.

Debt Avalanche Method: Pay minimums on all debts, but put extra money toward the debt with the highest interest rate first. This method minimizes the total interest you pay over time.

Both methods work—choose the one that best matches your personality and financial situation.

How to Use Proculator Calculators for Loan Planning

Proculator offers a set of free calculators that make loan planning interactive and simple. Here are a few recommended flows:

- Estimate affordability: Use the Loan Calculator and Mortgage Calculator. Input different loan amounts, interest rates, and terms to find a payment that fits your budget.

- Plan extra payments: Try the Home Loan Prepayment Calculator. See how even small additional payments can reduce your loan term and total interest.

- Budget impact: Use the Salary After Tax Calculator to check net income vs EMI burden. Ensure your total debt payments don't exceed 36% of your gross monthly income.

- Compare investments vs prepaying: Use Compound Interest Calculator to see when investing beats prepaying a low-rate loan. If your loan interest rate is lower than potential investment returns, investing might make more sense.

- Plan for future purchases: Use the Saving Goal Calculator to determine how much you need to save monthly for a down payment.

Real-World Example (Illustrative)

Suppose you take a $100,000 home loan for 20 years at 6% annual interest. Monthly interest rate r = 0.06/12 = 0.005. Using the EMI formula above produces a monthly payment (EMI) of roughly $716. You can plug these numbers into Proculator's Mortgage Calculator to see a full amortization table and to simulate extra payments.

If you make an additional $100 monthly payment, you will reduce the total interest paid and shorten the loan term — model this with our Prepayment Calculator.

Let's break down the numbers:

| Scenario | Monthly Payment | Total Interest | Loan Term | Total Cost |

|---|---|---|---|---|

| No extra payments | $716 | $71,869 | 20 years | $171,869 |

| With $100 extra monthly | $816 | $56,284 | 16 years | $156,284 |

| Savings | - | $15,585 | 4 years | $15,585 |

As you can see, an extra $100 per month saves you $15,585 in interest and allows you to own your home 4 years earlier. This demonstrates the powerful impact of even modest additional payments.

Loan Mistakes to Avoid

- Ignoring total interest and focusing only on monthly EMI. A longer term might mean lower monthly payments but significantly more interest over time.

- Not checking for prepayment penalties before paying extra. Some loans charge fees for early repayment that could negate your interest savings.

- Choosing a very long term to reduce monthly cashflow but increasing lifetime interest. Always consider the total cost of the loan, not just the monthly payment.

- Failing to include insurance and maintenance costs (for mortgages) in affordability checks. Homeownership comes with additional expenses beyond the mortgage payment.

- Borrowing more than you need just because you qualify for it. More debt means more interest and longer repayment periods.

- Not shopping around for the best rates. Even a small difference in interest rates can save you thousands over the loan term.

- Ignoring your credit score before applying. A better credit score can qualify you for significantly lower interest rates.

- Not reading the fine print. Understand all terms, conditions, and fees before signing any loan agreement.

Checklist Before You Sign a Loan

- Verify the APR and total cost of the loan, not just the interest rate.

- Ask for the amortization schedule and run it in a calculator to understand how payments are allocated.

- Understand fees and penalties for late payment and prepayment.

- Confirm whether rate is fixed or variable and how often it adjusts if variable.

- Keep an emergency fund of 3–6 months of expenses before taking large debt.

- Check if you can comfortably afford the payment alongside your other financial obligations.

- Read all terms and conditions carefully, paying special attention to fine print.

- Consider getting pre-approved to strengthen your negotiating position.

- Check for any discount opportunities (autopay discounts, relationship discounts with your bank).

- Understand the process for requesting deferment or forbearance if needed.

Success Tip: Create a loan comparison worksheet that includes all relevant factors: interest rate, APR, term, monthly payment, total cost, fees, and special features. This will help you make an apples-to-apples comparison between loan offers.

Conclusion

Loans are powerful financial tools when used responsibly. By understanding interest, using calculators to model different scenarios, and applying smart repayment strategies, you can minimize interest costs and pay off debt faster. Explore Proculator's suite of calculators to plan and track your loan decisions.

Remember that the best loan is one that helps you achieve your financial goals without creating undue stress or burden. Whether you're buying a home, financing education, or consolidating debt, informed borrowing decisions will serve you well throughout your financial journey.

The key takeaways are:

- Understand the true cost of borrowing by looking at APR, not just interest rate

- Make extra payments when possible to reduce total interest and shorten loan term

- Use calculators to model different scenarios before committing

- Shop around for the best terms and read all fine print carefully

- Prioritize high-interest debt and consider strategic repayment methods