Compound interest allows your money to grow exponentially over time

Compound Interest: The Complete Guide to Growing Your Wealth Exponentially

Discover how compound interest works, why Einstein called it the "eighth wonder of the world," and how to harness its power for financial freedom.

Table of Contents

The Power of Compound Interest

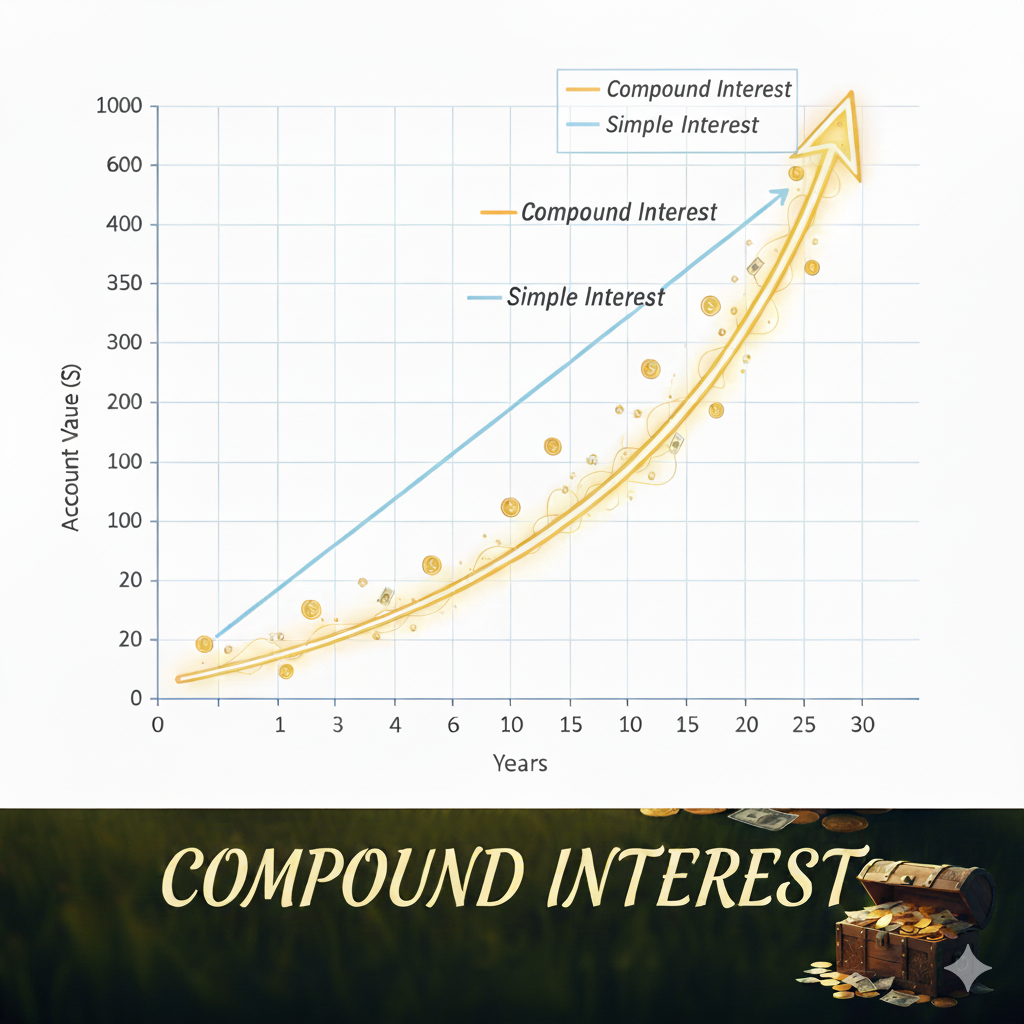

Compound interest is the financial phenomenon where your interest earns additional interest over time, creating exponential growth. Unlike simple interest (which grows linearly), compound interest accelerates your wealth accumulation in a snowball effect.

Exponential Growth Curve

Your money grows faster as time passes because you earn returns on both your principal and accumulated interest.

Time Magnifies Results

Starting just 5 years earlier can increase your final balance by 30-50%. Use our calculator to see the difference.

Regular Contributions Supercharge Growth

Adding money periodically provides more principal that compounds over time. Even small increases make a big difference.

Real Example:

A $10,000 investment at 7% annual return grows to $76,123 in 30 years without adding another dollar. That's $66,123 earned purely from compounding!

The Math Behind Compound Interest

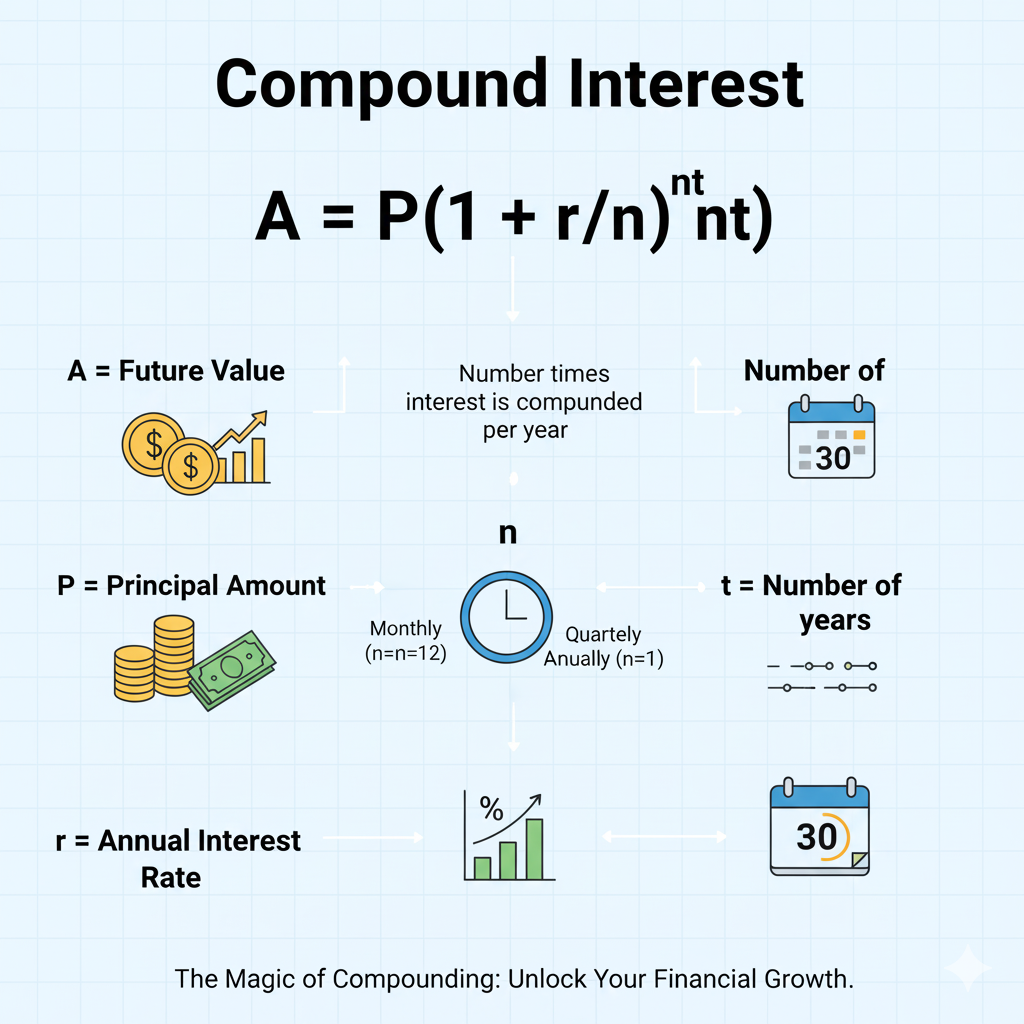

The Compound Interest Formula

A = P(1 + r/n)nt

Where:

A = Final amount

P = Principal amount ($)

r = Annual interest rate (decimal)

n = Compounding periods per year

t = Time in years

This formula shows how compounding frequency (n) and time (t) exponentially grow your money.

Compounding Frequency Matters

| Frequency | Periods/Year | $10,000 in 30y @7% |

|---|---|---|

| Annually | 1 | $76,123 |

| Quarterly | 4 | $80,496 |

| Monthly | 12 | $81,998 |

| Daily | 365 | $82,453 |

Pro Tip:

While compounding frequency matters, time and rate have far greater impact. Focus on starting early and earning higher returns when possible.

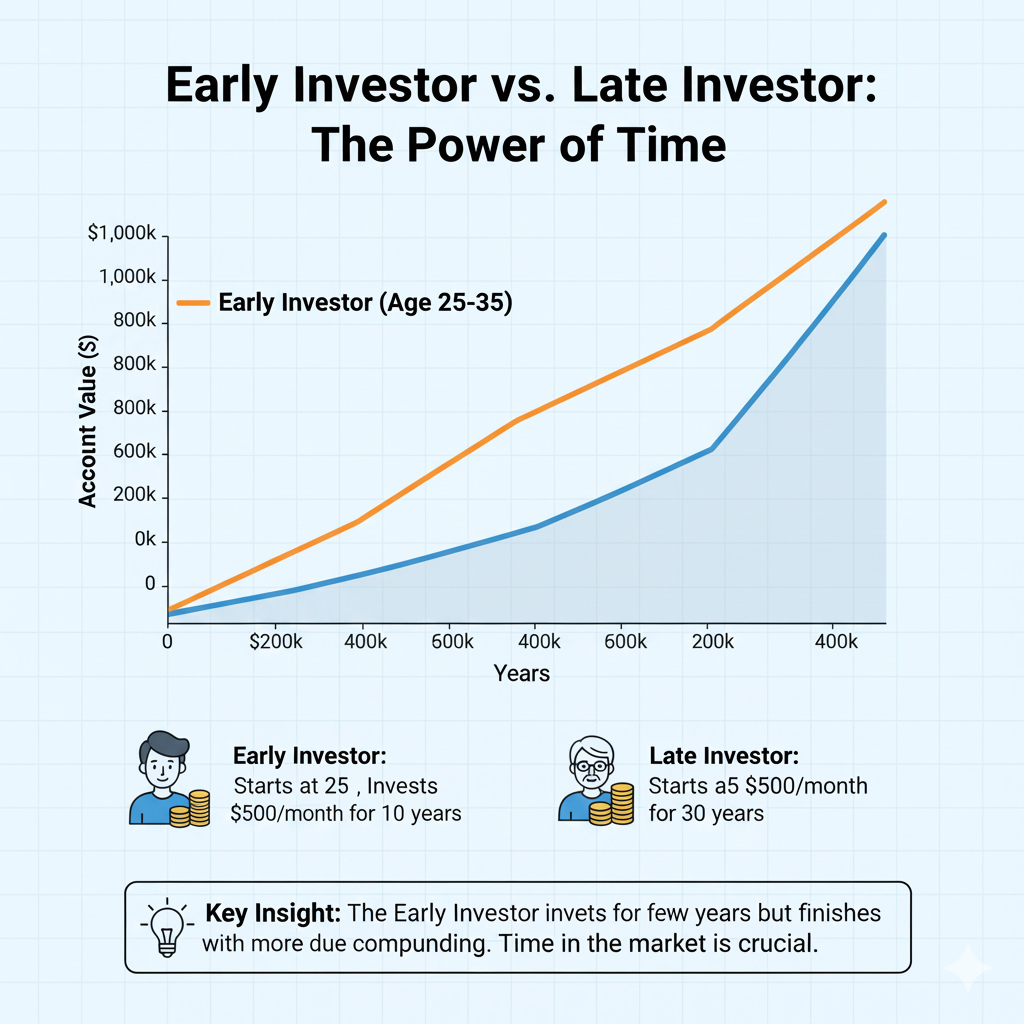

Compound Interest in Action: Comparative Scenarios

See how different approaches lead to dramatically different outcomes over time.

Visualizing the dramatic difference starting early makes in investment outcomes

The Early Bird vs. The Late Starter

Both invest $300/month at 7% return. Starting just 10 years earlier more than doubles the final balance!

Calculate your scenario →Consistency Pays Off

Investing half as much for twice as long yields more than double the result thanks to compounding.

Plan your savings →| Scenario | Initial | Monthly | Rate | Years | Total Invested | Final Value | Growth |

|---|---|---|---|---|---|---|---|

| Conservative | $5,000 | $200 | 5% | 30 | $77,000 | $183,928 | +139% |

| Moderate | $5,000 | $500 | 7% | 25 | $155,000 | $417,863 | +170% |

| Aggressive | $10,000 | $1,000 | 9% | 20 | $250,000 | $747,732 | +199% |

Note: These examples assume monthly compounding and reinvestment of earnings. Actual results will vary based on market conditions and specific investments.

7 Proven Strategies to Maximize Compound Growth

Implement these evidence-based approaches to supercharge your wealth building.

Start Yesterday

Every year you delay costs you thousands in lost compounding. A 25-year-old investing $300/month at 7% until 65 will have ~$1.14M. Starting at 35 yields just $540k - less than half!

Automate Contributions

Set up automatic transfers to investment accounts right after payday. Those who automate save 3x more than those who don't, according to a Vanguard study.

Optimize Account Types

Use tax-advantaged accounts like 401(k)s and IRAs first. The tax savings effectively boost your returns by 20-40% depending on your bracket.

Reinvest All Earnings

Enable dividend reinvestment (DRIP) in all accounts. Over 30 years, reinvested dividends account for 60-80% of total returns in the stock market.

Minimize Fees

A 1% fee can consume 30% of your potential returns over 30 years. Choose low-cost index funds (expense ratios < 0.2%) to keep more money compounding.

Increase Contributions Gradually

Boost savings by 1% of salary each year or 50% of raises. Small increases are painless but dramatically impact final balances due to compounding.

Stay the Course

The average investor earns just 2.9% annually due to emotional decisions (Dalbar study). Staying invested through market cycles is crucial for compounding to work.

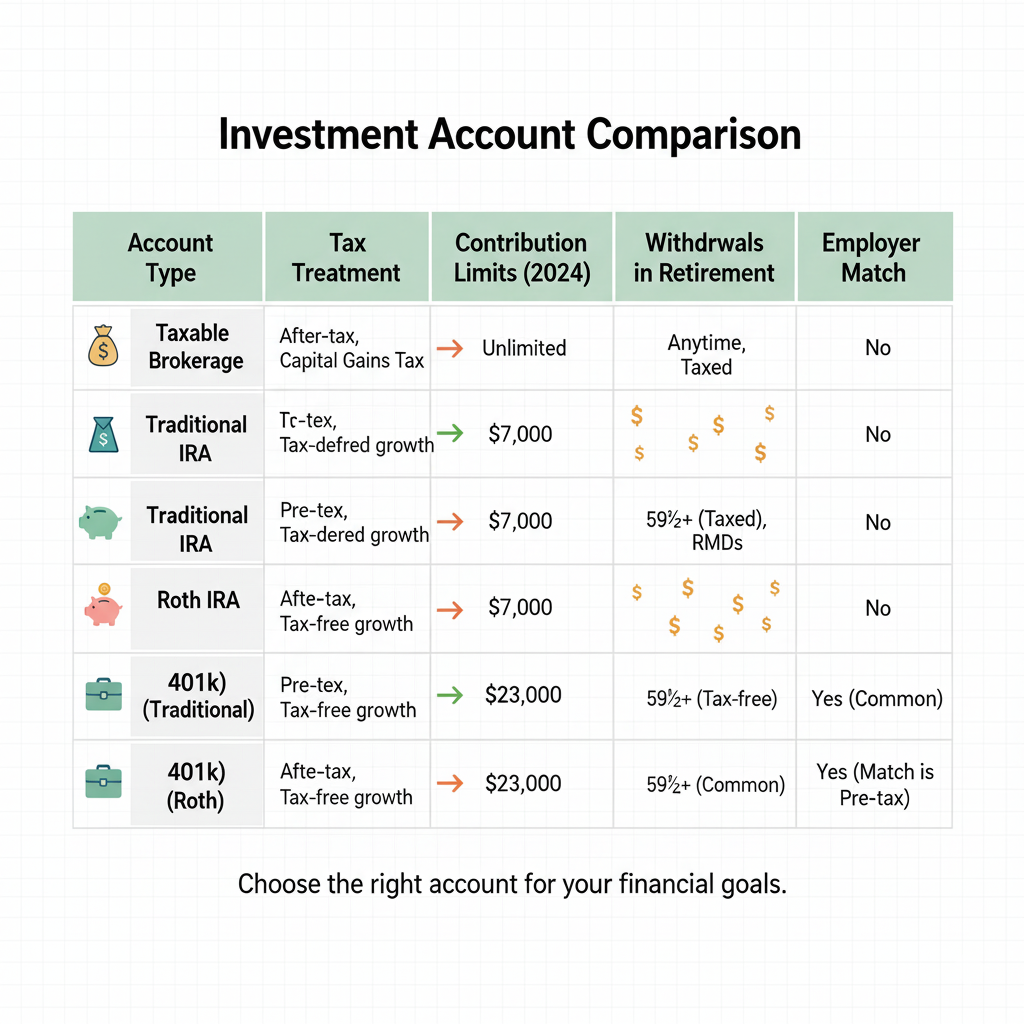

Where to Grow Your Money: Account Comparison

Different accounts offer various advantages for compound growth. Choose wisely based on your goals.

Comparing the features of different investment account types

Retirement Accounts

- 401(k)/403(b): Tax-deferred, employer matches boost compounding

- Traditional IRA: Tax deduction now, taxed later

- Roth IRA: After-tax money grows tax-free forever

Best for: Long-term retirement savings where you won't touch funds for decades.

Taxable Brokerage

- Flexibility: No contribution limits or withdrawal penalties

- Tax Efficiency: Long-term capital gains rates lower than income tax

- Diversification: Complements retirement accounts

Best for: Goals before 59½ or after maxing retirement accounts.

Education/Other Accounts

- 529 Plans: Tax-free growth for education expenses

- HSAs: Triple tax advantage for healthcare

- HYSA: Safe compounding for short-term goals

Best for: Specific goals like education or medical expenses.

5 Costly Compound Interest Mistakes to Avoid

1. Waiting to Start

Every year you delay costs you thousands. Investing $300/month from age 25-35 then stopping grows to more than starting at 35 and continuing until 65.

Solution:

Start with whatever you can today, even if small. Increase contributions over time.

2. Cashing Out Early

Withdrawing funds interrupts compounding. A $50,000 withdrawal at age 40 could mean $300,000+ less at retirement.

Solution:

Maintain separate emergency fund. Consider loans before withdrawals.

3. Ignoring Fees

2% annual fees can consume 40% of potential returns over 30 years through lost compounding.

Solution:

Choose low-cost index funds (expense ratios < 0.2%). Avoid unnecessary account fees.

4. Market Timing

Missing just the 10 best days in 20 years can cut returns in half, devastating compounding.

Solution:

Stay invested through cycles. Use dollar-cost averaging.

5. Not Increasing Contributions

Keeping contributions static despite rising income leaves thousands in potential compounding on the table.

Solution:

Automate annual increases (1% of salary or 50% of raises).

See Compound Interest Work for You

Our advanced calculator shows exactly how your money could grow with different contribution and return scenarios.

Try Our Compound Interest CalculatorExplore different scenarios and start planning your financial future today.

Compound Interest FAQs

How often is interest compounded?

It depends on the account. Savings accounts typically compound daily, while investment accounts compound as dividends/interest are paid (often quarterly). The more frequent the compounding, the slightly higher your returns.

Can compound interest work against me?

Absolutely. Debt compounds just like investments. Credit cards charging 18% APR can quickly spiral if you only make minimum payments. Always prioritize high-interest debt.

What's a realistic return rate to assume?

After inflation, a diversified stock portfolio averages 6-7% annually long-term. Conservative investors might use 4-5%, while very aggressive investors might project 8-9%. Be cautious with higher assumptions.

How do taxes affect compounding?

Taxes can significantly impact compounding, which is why tax-advantaged accounts are so powerful. In taxable accounts, you lose some compounding to taxes each year on dividends and realized gains.

Financial Disclaimer

This content is for educational purposes only and does not constitute financial advice. The projected results are hypothetical and don't guarantee future performance. Investment returns are not guaranteed and may fluctuate. Past performance is not indicative of future results. Consult with a qualified financial advisor before making investment decisions. All investments involve risk, including possible loss of principal.